Institutional Insights: Credit Agricole FX Weekly 4/725

Fiscal Dominance in FX Markets

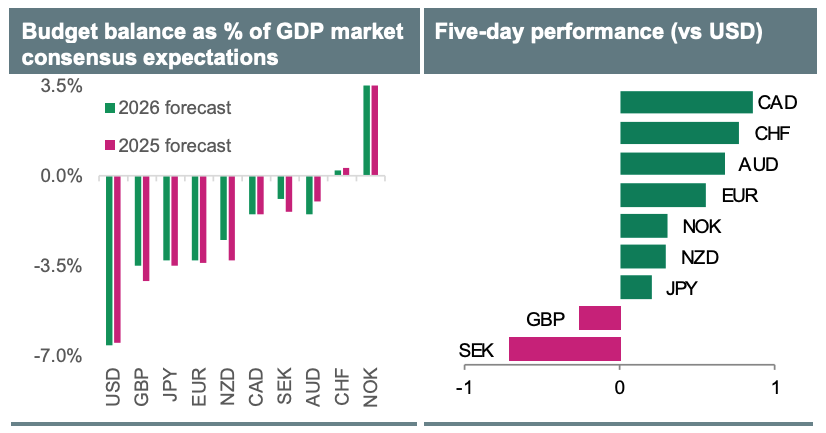

July marks a year since UK Prime Minister Keir Starmer assumed office and six months into US President Donald Trump’s second term. The market response to Labour’s first year in power and Trump’s continued leadership has been mixed. While UK and US stock markets recently reached record highs, the British pound (GBP) has been the weakest-performing European G10 currency, and the US dollar (USD) has been the worst-performing G10 currency overall this year.

A key factor behind these developments has been government efforts to address fiscal challenges. In the UK, attempts to increase healthcare spending while avoiding further fiscal strain have faltered, with failed welfare cuts likely leading to impending tax hikes. Meanwhile, the US administration has sought to maintain low personal income tax burdens, relying instead on trade tariffs and spending cuts to stabilize fiscal revenues.

These policies have not alleviated market concerns about the long-term fiscal health of either country. On the contrary, they have exacerbated economic growth challenges and heightened fears of fiscal dominance, particularly in the US. This has led investors to adopt a more dovish stance on the Bank of England (BoE) and the Federal Reserve (Fed), reducing the appeal of both the GBP and USD in recent weeks. In contrast, the euro (EUR) has gained support, buoyed by expectations of fiscal stimulus in Germany, where fiscal flexibility remains strong.

Following the passage of Trump’s fiscal stimulus bill, attention will turn to the upcoming trade deal deadline on 9 July. It remains uncertain whether the US can finalize agreements with all its trading partners by this date. Investors will weigh the potential benefits of any completed deals against the negative economic impact of tariffs, especially if the deadline is extended. Additionally, the release of May UK GDP data next week will offer more details about the economic repercussions of Starmer’s fiscal policies.

Elsewhere, softening inflation, weaker labor market data, and the limited impact of earlier rate cuts on consumption are likely to prompt the Reserve Bank of Australia (RBA) to lower its cash rate by 25 basis points to 3.60% next week. However, Governor Michelle Bullock may push back against aggressive market expectations for additional cuts. Meanwhile, with New Zealand’s economy showing signs of recovery and inflation risks resurfacing, the Reserve Bank of New Zealand (RBNZ) is expected to hold rates steady at its upcoming meeting, marking a pause in its easing cycle.

FX and Gold Outlook

EUR/USD Outlook

While we have recently adopted a more positive short-term view on EUR/USD, we see limited potential for significant EUR gains from current levels in 2025. We anticipate renewed EUR/USD weakness in 2026. Recent EUR strength has been supported by market expectations of diversification away from the USD and optimism around aggressive fiscal stimulus bolstering the Eurozone’s economic outlook, potentially attracting capital inflows. These factors may continue to support EUR/USD for the remainder of the year. However, much of this optimism appears to be priced in, as indicated by our short- and long-term fair value models, which could cap further gains and underscore growing downside risks for the EUR over the next 6 to 12 months.

USD Outlook

The USD outlook for 2025 remains subdued due to concerns about (1) economic damage and portfolio rebalancing triggered by the policies of the Trump administration, and (2) the long-term fiscal implications of Trump’s stimulus package and the need to raise the debt ceiling. However, we do not foresee a USD collapse. The negative economic impact of these policies is expected to be significant but temporary. The US economy could begin recovering in the second half of 2025, rebounding in 2026 as fiscal stimulus takes center stage. This recovery could allow the Federal Reserve to avoid aggressive policy easing, especially if inflation remains persistent. We do not anticipate the USD losing its reserve currency status and expect the USD to recover within 6 to 12 months.

EUR/CHF Outlook

The CHF has strengthened due to demand for safe havens amidst tariff uncertainties, even outperforming the resurgent EUR. While EUR/CHF may rise modestly this year, the return of zero interest rate policy (ZIRP) in Switzerland makes the CHF an attractive funding currency. However, lower inflation differentials and stable growth may temper CHF real valuations, helping to avoid significant nominal losses.

JPY Outlook

We remain skeptical of major trade agreements between the US and its trading partners, positioning the JPY as a strong hedge against potential US stagflation. Asset managers are likely to continue diversifying away from US and Japanese assets, benefiting the JPY. However, USD/JPY faces downward pressure as the Fed cuts rates and the Bank of Japan potentially raises rates in 2026.

GBP Outlook

The GBP is expected to outperform both the EUR and USD in 2025 and beyond, partly due to reduced trade tensions with the US and EU. Persistent UK inflation could delay aggressive Bank of England rate cuts, maintaining the GBP’s rate advantage over the EUR. Additionally, recent GBP underperformance has placed it in undervalued territory relative to the EUR, according to our short-term FX fair value model. However, concerns over the UK government’s fiscal conservatism reputation present a downside risk to the GBP’s near-term outlook.

USD/CAD Outlook

USD/CAD has returned to levels near 1.36, primarily due to broad USD selling. This retracement exceeds what relative rates would suggest. Any trade agreement between the US and Canada could act as a catalyst for a potential pullback in spot prices.

AUD and NZD Outlook

Investor concerns about US tariffs and a global trade war have likely peaked. A narrowing of trade conflicts to the US-China relationship is less detrimental to the AUD than a broader trade war. China’s ongoing economic stimulus to counteract US tariffs is expected to benefit the AUD, given its strong correlation with the CNY. Australia’s labor market remains tight, supporting inflation and reducing the likelihood of aggressive rate cuts, while post-election government spending adds further support.

New Zealand’s economy is recovering strongly from a deep recession, driven by robust agricultural export prices and production. While the lack of major US trade deals could weigh on the NZD, diversification away from US assets will be a tailwind for NZD/USD, which is positively correlated with relative Asia-US equity market performance.

NOK and SEK Outlook

The NOK continues its gradual recovery, supported by Norway’s strong economic fundamentals and regained rate appeal, assuming no global disruptions. Meanwhile, the SEK has been the G10 FX outperformer year-to-date, benefiting from its high-beta EUR proxy status. However, a softer economic outlook and potential monetary easing may limit SEK gains unless Sweden demonstrates clear macroeconomic outperformance relative to the Eurozone.

Gold Outlook

Recent aggressive gains in gold prices may deter buyers in the near term. However, gold’s strength is likely to resume in the next three to six months, driven by central bank purchases and the possibility of the Federal Reserve resuming its easing cycle, which could push US real rates and the USD lower. A significant rebound in the US economic outlook, along with higher interest rates and Treasury yields, would be required to challenge gold’s strength in 2026.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!