FTSE 100 FINISH LINE 11/5/26

FTSE 100 FINISH LINE 11/5/26

Starmer Reset Fails to Clear the Tape

The FTSE 100 ended little changed to modestly firmer, but the index level flattered a market still trading with a clear UK political-risk overlay. Investors came in focused on Keir Starmer’s reset speech after Labour’s bruising local-election performance, with Reform’s surge and pressure from within Labour keeping gilts, sterling and domestic cyclicals on watch. The message from the tape was not panic, but no clean relief rally either: the market wants evidence that Downing Street can stabilise the party, defend fiscal credibility and avoid a policy lurch that would reprice UK borrowing risk.

The political read-through was most visible in the domestically exposed parts of the market. Housebuilders, banks, retailers, and utilities acted as indicators of confidence in the UK policy mix, with investors reacting to any sign that Labour might respond to electoral pressure with more interventionist or fiscally loose measures. Rising borrowing-cost headlines also mattered: a higher gilt-risk premium is unhelpful for rate-sensitive stocks and makes the FTSE’s domestic laggards harder to re-rate, even when the headline index is supported by global earners.

Single-stock news kept dispersion high. IAG remained in focus after last week’s profit disappointment and warning on higher jet-fuel costs, leaving airlines exposed to both Middle East risk and margin pressure. Intertek continued to trade around bid speculation after rejecting EQT’s sweetened approach, with investors weighing the loss of near-term takeover support against the possibility of further private-equity interest. Meanwhile, the oil majors offered some index support as crude stayed elevated, but the market is increasingly treating higher energy as a tax on consumers and corporate margins, not just a windfall for BP and Shell. Shares of Compass Group rose 4.8% to $30.92, making it one of the top gainers on the FTSE 100, which is up 0.23%. The company expects full-year adjusted operating profit growth to exceed 11%, an increase from the previous forecast of around 10%. It remains confident in achieving mid-to-high single-digit organic revenue growth in the long term. For H1, adjusted operating profit increased by 12% to $1.84 billion, prompting an upward revision of the full-year profit forecast. However, the stock is down approximately 5.37% year-to-date.

Finish line: this was a politics-first FTSE session dressed up as a quiet index move. Starmer’s attempt to reset the narrative has not yet reset investor confidence, and the market is demanding proof rather than promises. Until Labour’s internal pressure eases, gilt volatility cools and single-name disappointments stop landing, the FTSE’s rallies are likely to remain narrow, tactical and stock-specific – with global defensives favoured and UK domestic beta still on a short leash.

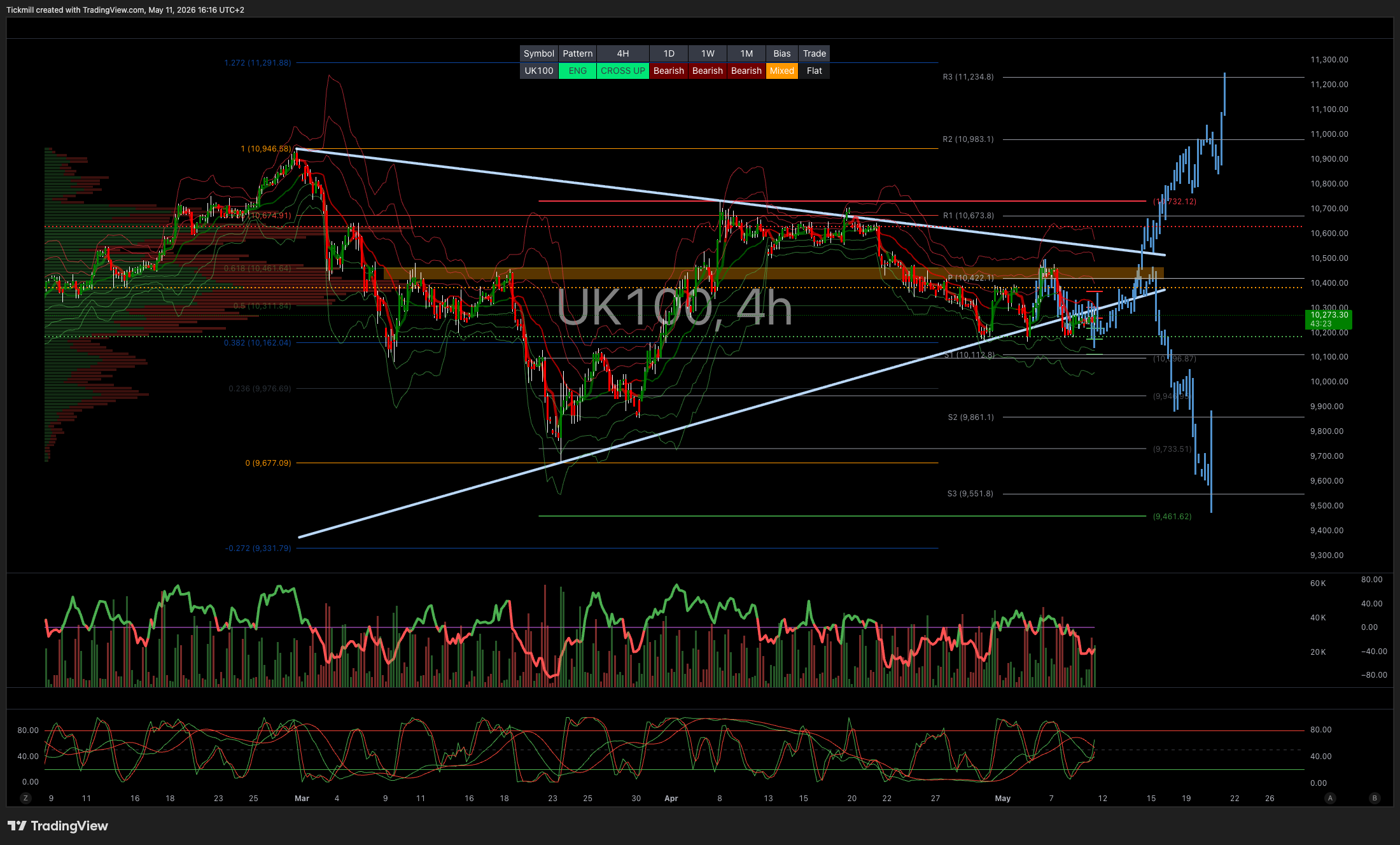

TECHNICAL & TRADE VIEW – FTSE100

Daily VWAP Bearish

Weekly VWAP Bearish

Above 10500 Target 11000

Below 10100 Target 9469

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!